Aadinath Agro Industries ., In re

Date: May 22, 2025

Subject Matter

Cumulative Tax Payments Don't Waive GST Rule 86B ITC Restriction

Summary

Facts of the Case: A partnership firm, Aadinath Agro Industries, engaged in spice processing, has a monthly taxable turnover exceeding ₹50 lakh, thus subject to restrictions under Rule 86B of the CGST Rules, 2017. The total income tax paid by the firm and its partners during the financial year 2023-24 is ₹1,04,427, but no individual partner has paid more than ₹1 lakh.

Key Issues: The firm seeks clarity on whether the cumulative tax payment of the firm and its partners can be considered for the exemption under Rule 86B and whether the exemption applies if no single partner has paid more than ₹1 lakh.

Arguments:

- Financial Interdependence: The firm argues that as partners share the profits, their financial standings should be assessed together for tax compliance.

- Legislative Intent: The introduction of Rule 86B aims to combat tax evasion and fraudulent claims. The firm argues those fulfilling their tax obligations should not face undue restrictions.

- Ambiguity in Rule Wording: The applicant highlights a lack of clarity on whether the ₹1 lakh threshold applies per partner or cumulatively.

Ruling: The Advance Ruling Authority concluded:

- Total Tax Consideration: The total income tax paid by the firm and its partners cannot be considered for the exemption under Rule 86B.

- Individual Partner's Tax Liability: The collective tax cannot be used to fulfill the conditions for exemption, as each partner must individually meet the ₹1 lakh requirement.

- The restriction under Rule 86B remains applicable to the firm, thus limiting the utilization of input tax credit as per the outlined rules.

In essence, the ruling underscores that individual compliance, rather than collective compliance, dictates the exemption eligibility under Rule 86B of the CGST Rules.

FULL TEXT OF THE ORDER OF AUTHORITY FOR ADVANCE RULING, RAJASTHAN

A. SUBMISSION OF THE APPLICANT(iii brief):-

Brief’ Facts of case:

- I he applicant, 1: cadinath Agro IHdustriesl, is a partnership firm engaged in [Spice processing unit] and is registered under GS’l’.

- The firm’s monthly taxable turnover exceeds Z50 lakh, making it subject to Rule 86B restrictions.

- The total inicoirie tax in the preceding financial year is as f011ows: r’age 1 of 11

| Entity/Partner | Income Tax Paid (₹) | Financial Year |

| The Firm | [ 0.00] | [FY 2023-24] |

| Partner 1 | [32,274.00] | [FY 2023-24] |

| Partner 2 | [72,153.00] | [FY 2023-24] |

| Partner 3 | [0.00] | [FY 2023-24] |

| Total (Firm + Partners) | [1,04,427.00] | |

- Although no individual partner has paid more than Rs. 1 lakh the firm and its partners together have paid well above Rs. 1 lakh in income tax.

B. INTERPRETATION AND UNDERSTANDING OF APPLICANT ON QUESTION RAISED (IN BRIEF)

- Issue for Consideration:

o Whether the cumulative tax payment of the firm and his partners can be considered for the exemption under Rule 86B?

0 Whether the firm qualifies for exemption, even if no single partner has paid more than Rs. 1 lakh individually?

4. Arguments Supporting the Cumulative Consideration of Tax Paid 4.1. Partnership Firms and Partners Are Financially Interdependent

4.1 A partnership firm is a tax-paying entity. but its profits are ultimately distributed to partners, either through profit share or remuneration.

- Income tax is either paid at the firm level or at the partner level, meaning the financial sianding of the firm and its partners is interlinked.

- Denying the exemption simply because no individual partner paid ZI lakh contradicts the economic reality of partnership taxation.

- Under Partnership Act, a partnership firm is treated as an aggregate of partners, and the firm’s income is ultimately taxed in the hands of partners.

- Though a firm and its partners arc distinct under the Income Tax Act, 1961, they operate as a single economic unit.

- Just as companies and their directors are financially assessed together, partnerships should also be evaluated on a combined tax compliance basis.

- A partnership firm and its partners are not entirely separate for tax purposes.

- The income of a partnership firm ultimately flows to its partners. either through profit distribution or remuneration or interest on capital.

- if a firm pa):s substantial income tax, it reflects the financial credibility of the partners as well, since they are the ultimate beneficiaries.

- If a firm and its partners collectively pay substantial income tax, they are genuine tax-compliant businesses and should not lace unnecessary cash restrictions. Since the firm and its partners are jointly liable for taxation, the total tax paid by all partners together should be considered for exemption. and not just the tax paid by a single partner.

Example Scenario:

- A firm pays ₹50000 lakh in tax. while two partners pay ₹50,000 each.

- Total tax paid = 21.5 lakh, yet exemption is denied because no single partner paid Rs. 1 lakh.

- This creates undue hardship for genuine businesses and contradicts the exemption’s intent.

4.2. Legislative intent of Rule 86B — Preventing Fake llTC Claims

Rule 8613 of the CGS”!’ Rules, 2017 was introduced vide Notification No. 94/2020 —Central Tax, dated 22nd December 2020, and became effective from 1st January 2021. The primary objective behind the introduction of Rule 868 was to curb tax evasion, fraudulent ITC claims, and bogus invoicing under GST.

Key Reasons for ‘Introducing Rule 861 :

- Curbing Fake ITC Utilization and Tax Evasion

Before the introduction of Rule 8613, many businesses were fraudulently utilizing 100% of their Input Tax Credit (ITC) without paying any actual tax in cash. This led to revenue leakage for the government. Bogus firms were created solely to claim 1″1 C without real business operations. Rule 86B prevents excessive reliance on ETC by mandating at least l’Yo of the output tax liability to be paid in cash.

- Discouraging Circular Trading and Fake Invoicing

Many fraudulent businesses were engaged in circular trading, where fake invoices were generated without actual supply of goods or services, solely for passing ITC. This artificial ITC was then used to reduce actual tax liability to zero. Rule 868 forces high-turnover taxpayers to make some cash payments, making such fraud more difficult.

- Increasing Government Revenue and Compliance

13y ensuring that at least 1% of GST liability is discharged in cash, the government aims to improve cash flow in the tax system and reduce dependency on paper-based tax credits. This also ensures that only genuine businesses with real transactions can fully utilize their ITC.

- Strengthening GST Audit and Monitoring

The rule acts as an automatic filter to flag risky taxpayers. Businesses that frequently claim 100% 1TC utilization without cash payments are now subject to stricter scrutiny. This helps tax authorities detect and prevent ITC fraud early.

- Genuine businesses that are paying substantial taxes should not be unnecessarily burdened by cash payment restrictions.

- Ila partnership firm and its partners collectively pay more than 1 lakh in income tax, it proves their genuine tax compliance, fulfilling the spirit of the exemption

4.3. Ambiguity in the Wording of Rule 86B

- The exemption applies if:

“Any of its two partners have paid more than Rs. 1 lakh…”

- The rule does not explicitly state whether the ₹1 lakh threshold applies to each partner separately or cumulatively.

- Ambiguities in taxation laws must be interpreted in favor of the taxpayer (Supreme Court ruling in CIT Vegetable Products Ltd., 1973).

- The Advance Ruling Authority should provide clarity on whether the exemption can be granted based on combined tax payments.

- The law should be interpreted in a manner that supports honest taxpayers rather than creating rigid compliance hurdles.

- In corporate taxation, a company’s tax compliance and that of its directors are often considered

- In bank loan approvals, a firm’s and its partners’ financial standings are assessed Jointly.

- UST laws should align with these principles and recognize the firm-partner financial nexus.

- Many global tax systems consider partnerships and their stakeholders as financially interdependent.

- Denying cumulative tax consideration creates an uneven playing field For partnerships compared to sole proprietorships and companies.

Additional Submission:–

SUBMISSION FOR PERSONAL HEARING BEFORE AAR

Applicant: Aadinath Agro Industries

GS TIN: 08ABXFA7290E1ZX

Subject: Advance Ruling on Applicability of Rule 8611 of CGS’!’ Rules, 2017

1. Introduction

This submission is made on behalf of M/s Aadinath Agro Industries, a partnership firm registered under the Goods and Services ‘l’ax Act, having its place of bu’siness in Rajasthan. The firm is engaged in the business of spice manufacturing and trading, contributing significantly to the supply chain in the FIVICG sector. The firm’s monthly taxable turnover exceeds Rs. 50 lakhs, thereby prima facie making Rule 8611 applicable.

2. Facts of the Case

The key facts relevant to the present matter are as follows:

-The monthly taxable turnover of the firm exceeds Rs. 50 lakhs.

-The firm primarily operates through the Input Tax Credit (ITC) mechanism.

-Rule 8613 of the CGST Rules, 2017 mandates that only 99% of the output tax liability can be discharged through ITC.

-An exemption exists for entities where the proprietor, Karta, MI), or any two partners have paid income tax exceeding Rs.1,00,000 in each of the last two financial years.

| Financial year | Partner 1 | Partner 2 | Partner 3 | Firm | Total |

| 2022-23 | 48,766.00 | 90,072.00 | 0.00 | 0.00 | 1,38,838.00 |

| 2022-23 | 32,274.00 | 72,153.00 | 0.00 | 0.00 | 1,04,427.00 |

3. Rule 8613 — Text and Interpretation

Rule 8613 was introduced to prevent fraud and misuse of the input tax credit. It provides that registered persons shall not use ITC to discharge more than 99% of their output tax liability if the value of taxable supply (excluding exempt and zero-rated supply) exceeds Rs. 50 lakhs in a month.

Proviso to Rule 8613: Provides various exemptions, notably where the income tax paid by specified persons exceeds Rs. 1,00,000 in each of the two preceding financial years.

I he applicant submits that the cumulative income tax paid should he considered for exemption eligibility under this rule.

4. Grounds for Seeking Exemption

-Liberal Interpretation: The language “any of its two partners” must he read with the intent of identifying tax credibility, which can be satisfied cumulatively.

-Substance Over Form: The firm and partners are fiscally interlinked.

-Economic Contribution: The firm has significantly contributed to revenue through GS’l’.

-Deterrent Against Misuse vs. Harassment: The rule must not penalize honest taxpayers.

5. Applicability of Section 40(b) of Income Tax Act

Interest @ 12 percent on Partner’s Capital and Remuneration paid to partners is governed by Section 40(b) and is allowed as a deduction from the firm’s income:

Calculation of Remuneration:

-On the first Rs. 3,00,000 of book profit: 90% or Rs. 1,50,000 whichever is higher

-On balance: 60%

The partners’ remuneration and interest is taxable in their individual hands and profit share is taxable in Partnership firm thus exempt in their individual hands.

This shows that taxes paid by partners are directly attributable to income derived from the firm, justifying consideration of their tax payments for Rule 8613.

6. Tax Calculations of individual partners and firms: –

The tax liability (based on the provisional financial statements) of individual partners on the income derived from the partnership firm for the FY 2024-25 as per applicable tax regime/slab will be: –

Distribution of profit of Partnership firm & tax liability are as follows-

The total income tax paid by all the partners and firm cumulative is more than-one lakh which comes to 162683.00

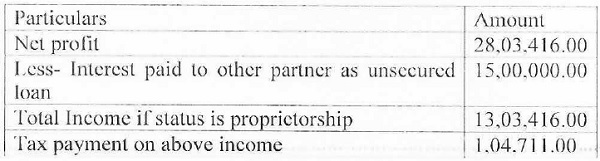

Now, if we consider a hypothetical situation that our firm’s status will be proprietorship instead of partnership firm then the total income tax payment made by our firm will be:

If any one partner becomes the proprietor of firm, then the tax liability in his individual hand will be: –

It can be clearly seen than in case of partnership firm total income tax liability is higher than income tax liability of proprietorship firm Therefore, mere only our firm is constituted as partnership firm and total tax liability reduced to Rs. 40691.00 (firm only) the provisions of rule 86(b) applies on our firm. Thus, for applicability of rule 86(b) the total tax liability of both the firm and partners must be considered cumulatively.

7. Effect on the workingcapital requirement of firm: – Rule 8613 of the CGST Rules, 2017 mandates that certain taxpayers must pa.), at least 1% of their monthly GS'[‘ liability in cash, even if they have sufficient Input Tax Credit (ITC). This rule primarily affects our businesses as we have taxable turnover exceeding Z50 lakhs in a month and we also have sufficient input tax credit balance. Hie government introduced the rule with a motive to curb tax evasion and improve compliance but it has an adverse impact on working capital, especially when the 1% tax payment is required to paid even taxpayer has sufficient input tax credit balance. The rule introduced is affecting the business in following manner: –

- Cash Outflow Despite ITC Availability: Even if adequate ITC is available to offset the tax liability-, e must pay 1% in cash and this leads to blocking of funds, reducing liquidity.

- Increased Cost of Borrowing: To meet the cash requirement, we may need to rely on short-term borrowing, increasing their finance cost.

- Administrative Burden: Monthly compliance of the rule is necessary and that enhance the compliance cost and complexity.

- Impact on Margins: In low-margin businesses, even a 1% outflow can erode a significant portion of profits if the funds aren’t recovered or adjusted promptly.

The government of India is promoting business for MSME’s but the applicability of the above rule results in working capital strain and it is affecting the financial health and operational efficiency of businesses.

8. GST Input Credit — Early-Stage Utilization: We have initiated the manufacturing business operations in the FY 2024-25 therefore our business is new and we have significant Input Tax Credit (ITC) accumulated on account of capital expenditure, mostly related to the purchase of plant and machinery. As the business is still in its initial phase with limited outward taxable supplies, the utilization of the available ITC is progressing at a slower pace. Therefore, the accumulated FIV will be gradually offset against future GST liabilities based on the scale of operations and taxable turnover increases.

9. Legislative Intent and Policy Perspective

Rule 8613 was enacted to curb fraudulent practices involving fake invoicing and improper 1’C utilization. It was never intended to impact genuine businesses who regmlarly file returns, pay taxes and comply with law.

Clarificationfrom CBIC

Cl3IC via official communication and social media (e.g., Twitter – (a:ebic india) has clarified:

“The rule provides for various exemptions like exporters, suppliers of goods of inverted duty structure, taxpayers having a footprint in the Income Tax database etc. It is expected that this rule would be applicable to less than 0.5% of total taxpayer base of 1.2 crore…”

This clarification indicates that the rule is designed to target fraudsters and not compliant, tax-paying businesses such as the applicant.

10. Prayer

In view of the above, it is humbly prayed that:

-The cumulative income tax paid by partners and partnership firm be accepted as satisfying the exemption criteria.

-The applicant be granted exemption from the provisions of Rule 8613 of CGST Rules.

C. QUESTIONS ON WHICH THE ADVANCE RULING IS SOUGHT:

Questionl:Can the total income tax paid by the firm and its partners be considered for the exemption under Rule 8613?

Question2 :If no single partner has paid more than Zl lakh in tax, but the firm and partners together have, does the exemption still apply?

D. COMMENTS OF THE JURISDICTIONAL OFFICER: –

Comments from the jurisdictional officer has not received.

E. PERSONAL HEARING:

In the matter. personal hearing was granted to the applicant on 17.04.2025. Mr. Mukesh Chordiva (C.A.) Authorized Representative appeared Ibr personal hearing. They reiterated the submission already made by them. lie also submitted additional submission during personal hearing.

F. DISCUSSIONS AND FINDINGS

1) We have carefully examined the statement of facts, contents of the application filed by the applicant, submissions made at the time of hearing and the comments of the jurisdictional Tax Authority. We have also considered the issue involved, on which advance ruling is sought by the applicant and other relevant facts.

2) The applicant M/s Aadinath Agro Industries, a partnership firm registered under the Goods and Services Tax Act having GSTIN No. 08ABXFA7290E1ZX, and place of business at Plot No. B-109, RIICO Industrial Area, Bikaner Road, GOGELAV, NAGAUR-341001, Rajasthan. The firm is engaged in the business of spice processing and trading, contributing significantly to the supply chain in the FMCG sector. The firm’s monthly taxable turnover exceeds Rs.50 lakhs, making it subject to Rule 86B of CGST Rules, 2017 restrictions.

3) The present application has been filed by the applicant seeking clarification whether the cumulative income tax payment of the firm and its partners can be considered for the exemption under Rule 86B ibid and whether the firm qualifies for exemption, even if no single partner has paid more than 1 lakh individually.

4) We also found that the taxpayer has submitted that they are engaged in business of spice processing unit and their taxable turnover exceeds Rs.50 Lakh per month due to which restrictions of rule 86 B is applicable on them.

5) Further, we also found that Taxpayer has submitted the details of income tax paid by them in the preceding financial year i.e. FY 2023-24, which is as under:

| Entity/Partner | Income Tax Paid (₹) | Financial Year |

| The Firm | [ 0.00] | [FY 2023-24] |

| Partner 1 | [32,274.00] | [FY 2023-24] |

| Partner 2 | [72,153.00] | [FY 2023-24] |

| Partner 3 | [0.00] | [FY 2023-24] |

| Total (Firm + Partners) | [1,04,427.00] | |

From the above chart, the taxpayer submitted that no partner has paid income tax more than Rs. 1 lakh individually. However, the firm and its partners together have paid income tax above Rs. 1 lakh during the FY 2023-24. Further, the taxpayer submitted the details of total income tax paid by the firm and its partners during the FY 2022-23 and 2023-24, which is as under:

| Financial year | Partner 1 | Partner 2 | Partner 3 | Firm | Total |

| 2022-23 | 48,766.00 | 90,072.00 | 0.00 | 0.00 | 1,38,838.00 |

| 2022-23 | 32,274.00 | 72,153.00 | 0.00 | 0.00 | 1,04,427.00 |

6) Belbre proceeding, it is imperative to go through the relevant provision of the Rule 8613 ibid.

[Rule 8613. Restrictions on use of amount available in electronic credit ledger’

Notwithstanding anything contained in these rules, the registered person shall not use the amount available in electronic credit ledger to discharge his liability towards output tax in excess of ninety-nine per cent. of such tax liability, in cases where the value of taxable supply other than exempt supply and zero-rated supply, in a month exceeds .fifly lakh rupees:

Provided that the said restriction shall not apply where –

(a) the said person or the proprietor or karta or the managing director or any of its two partners, Iyhole-time Directors, Members I Managing Committee of Associations or Board of Trustees, as the case may he, have paid more than one lakh rupees as income tax under the Income-tax Act, 1961(43 of 1961) in each of the last two financial years for which the time limit to file return of income under subsection (1) Of section 139 of the said Act has expired; or

(b) the registered person has received a re fiend amount of more than one lakh rupees in the preceding financial year on account of unutilised input tax credit tinder clause (i) of first proviso of sub-section (3) of section 5-1, or

(c) the registered person has received a refund amount of more than one lakh rupees in the preceding financial year on account of unutilised input lax credit under clause (ii) of: first proviso of sub-section (3) of section or

(d) the registered person has discharged his liability towards’ output tax through the electronic cash ledger for an amount which is in excess of 1% of the total output tax liability, applied cumulatively, too the said month in the current financial year: or

(e) the registered person is –

(i) Government Department; or

(ii) a Public Sector Undertaking; or

(iii) a local authority; or

(iv) a statutory body:

7) Ongoing through the above rule, we found that rule 86B imposes restriction that the registered person shall not use the amount available in electronic credit ledger to discharge his liability towards output tax in excess of ninety- nine per cent of total tax liability, where the value of taxable supply other than exempt supply and zero-rate supply, in a month exceeds fifty lakh rupees.

8) In the present case, we found that the taxpayer himself submitted in his application that their monthly turnover is more than fifty lakh rupees. Therefore, as per the per Rule 86B, restriction to use amount available in electronic credit ledger upto ninety-nine percent of total tax liability is applicable on the taxpayer.

9) On further reading of the provision of Rule 86B, we observe that the restriction shall not apply, if any of its two partners of the firm have paid more than one lakh rupees as income tax under the Income-tax Act, 1961(43 of 1961) in each of the last two financial years. Further, the taxpayer has submitted the details of income tax paid by the firm and partners during the F.Y. 2022-23 and F.Y. 2023-24, which is as under:

| Financial Year | Partner 1 | Partner 2 | Partner 3 | Firm | Total |

| 2022-23 | 48,766.00 | 90,072.00 | 0.00 | 0.00 | 1,38,838.00 |

| 2023-24 | 32,274.00 | 72,153.00 | 0.00 | 0.00 | 1,04,427.00 |

From the above submission of the taxpayer, we found that neither the individual partner nor the firm has paid income tax more than ₹1 lakh during the last two financial years.

Further, we also observe that the taxpayer has raised question, whether the total income tax paid by the firm and its partners together can be considered for the exemption under Rule 86B. Ongoing through the provisions of Rule 86B ibid, we found that there is no provision of exemption for such conditions in the said rule where exemption can be consider for total income tax paid by the partners and the firm together.

In view of above, the exemption as per Rule 86B(a) is not applicable on the taxpayer. Hence, we hold that the restrictions of Rule 86B on the use of amount available in electronic credit ledger is applicable on the taxpayer. Thus, M/s Aadinath Agro Industries should use the amount available in electronic credit ledger to discharge his liability only up to ninety-nine per cent of total tax liability of the month as their monthly tax liability exceeds fifty lakh rupees and neither theindividual partner nor the firm has paid more than Rs. one lakh income tax during the last two financial years.

G. In view of the foregoing facts, circumstances and provisions of the GST law, we pass the following ruling.

RULING

Question 1: Can the total income tax paid by the firm and its partners be considered for the exemption under Rule 86B?

Ans 1- No, as discussed above.

Question2: If no single partner has paid more than l lakh in tax, but the firm and partners together have, does the exemption still apply?

Ms 2- No, as discussed above.