Dr. Meenakshi Agrawal Vs S. R. Lifesciences

Date: May 10, 2022

Subject Matter

Medical Store guilty of Profiteering

Summary

The Respondent has acted in contravention of the provisions of Section 171 of the CGST Act, 2017, and has not passed on the benefit of reduction in the rate of tax to his recipients by commensurate reduction in the prices. Accordingly, the profiteered amount is determined as Rs. 1,54,138/- as per the provisions of Rule 133 (1) of the CGST Rules 2017. The Respondent is therefore directed to reduce the prices of his products as per the provisions of Rule 133 (3) (a) of the CGST Rules, 2017, keeping in view the reduction in the rate of tax so that the benefit is passed on to the recipients. Accordingly, the Respondent is required to deposit the profiteered amount of Rs. 1,54,138/- along with the interest to be calculated @ 18% from the date when the above amount was collected by him from the recipients till the above amount is deposited in terms of Rule 133 (3) (b) of the CGST Rules, 2017. Since the other recipients (other than the Applicant No. 1), in this case, are not identifiable, the Respondent is directed to deposit the amount of profiteering of Rs. 1,53,138/- along with interest in the CWFs of the Central and Maharashtra State Government as per the provisions of Rule 133 (3) (c) of the CGST Rules, 2017 in the ratio of 50:50 along with interest @ 18% till the same is deposited.

1. The present Report dated 23.03.2020 has been received from the Director General of Anti-Profiteering (DGAP) after a detailed investigation under Rule 129 (6) of the Central Goods & Service Tax (CGST) Rules. 2017. The brief facts of the case are that the DGAP received a reference from the Standing Committee on Anti-profiteering on 09.10.2019 recommending a detailed investigation against the Respondent in respect of an application filed by the Applicant No. 1 under Rule 128 of the CGST Rules, 2017 alleging profiteering by the Respondent in respect of the supply of “ECLAT SERUM–. when the GST rate was reduced from 28% to 18% w.e.f. 15.11.2017. The Applicant No.1 has alleged that the Respondent had not passed on the benefit of reduction in the GST rate by the way of commensurate reduction in prices. The Applicant No. 1 had also submitted the copies of invoices of pre-rate reduction and post rate reduction prices of the product. The above application was initially examined by the Maharashtra State Screening Committee, which observed that the the Respondent had not passed on the appropriate benefits to his customers on account of reduction in tax rate and forwarded the complaint to the Standing Committee on Anti-profiteering for further action. The above application was examined by the Standing Committee on Anti-profiteering, in its meeting held on 13.09.2019, whereby it was decided to refer the same to the DGAP, to conduct a detailed investigation in the matter, in terms of Rule 129 of the CGST Rules, 2017.

2. The DGAP, on receipt of the aforesaid reference from the Standing Committee on Anti-profiteering, issued a Notice under Rule 129 of the Rules on 23.10.2019, calling upon the Respondent to reply as to whether he admitted that the benefit of ITC has not been passed on to his recipients by way of commensurate reduction in price and if so, to suo moto determine the quantum thereof and indicate the same in his reply to the Notice as well as to furnish all documents in support of his reply. Further. the DGAP allowed the Respondent to inspect the non-confidential evidence/information which formed the basis of the above Notice, during the period from 31.10.2019 to 01.11.2019. However, the Respondent did not avail of the opportunity.

3. The DGAP has stated that the Respondent did not furnish the complete records/ information and relevant documents which were required for investigation. Hence. three Summons dated 02.01.2020. 15.01.2020 and 03.02.2020 under Section 70 of the Central Goods and Services Tax Act, 2017 read with Rule 132 of the Rules, were issued to Sh. Suresh Mali. Proprietor of the Respondent, asking him to appear before the DGAP. In response, Sh. Suresh Mali, Proprietor of the Respondent appeared before the DGAP on 17.02.2020 and has submitted various documents/information in response to the above Notice and Summons vide his letters and emails dated 26.11.2019, 13.01.2020, 18.02.2020, 24.02.2020, 28.02.2020, 02.03.2020, 04.03.2020 and 05.03.2020, as furnished below:-

a) List of the all GSTIN Registration.

b) Copies of GSTR-1 & GSTR-3B returns for the period from November, 2017 to September, 2019 for all the GST registration in India.

c) Details of invoice-wise outward taxable supplies for the impacted products during the period July, 2017 to September, 2019.

d) Sample copies of invoices, pre and post 15.11.2017.

4. The Applicant No. 1 vide e-mail dated 13.03.2020, was also allowed to inspect the non-confidential documents/reply furnished by the Respondent on 16.03.2020 and 17.03.2020. However, the Applicant No. 1 did not avail of the same. The DGAP has reported that he has covered the period from 15.11.2017 to 30.09.2019 during the current investigation.

5. The DGAP has stated that he has examined the above application, the replies of the Respondent and the documents/evidence on record. The main issues for determination were whether the rate of GST on the products supplied by the Respondent was reduced from 28% to 18% w.e.f. 15.11.2017 and if so, whether such benefit had been passed on by the Respondent to his recipients by way of commensurate reduction in prices, in terms of Section 171 of the CGST Act, 2017.

6. The DGAP has further stated that the Central Government, on the recommendation of the GST Council, had reduced the GST rate on “the subject Goods” from 28% to 18% w.e.f. 15.11.2017, vide Notification No. 41/2017-Central Tax (Rate) dated 14.11.2017. The DGAP has also stated that on the examination of Section 171 of the Central Goods and Services Tax Act, 2017 which governed the anti-profiteering provisions under GST, Section 171(1) of the Central Goods and Services Tax Act, 2017 reads as “any reduction in rate of tax on any supply of goods or services or the benefit of input tax credit shall be passed on to the recipient by way of commensurate reduction in prices.” Thus, the legal requirement was abundantly clear that in the event of benefit of input tax credit or reduction in rate of tax, there must be a commensurate reduction in the prices of the goods or services. Such reduction could only be in monetary terms, so that the final price payable by a recipient got reduced commensurate with the reduction in the tax rate or benefit of input tax credit which was the legally prescribed mechanism to pass on the benefit of input tax credit or reduction in rate of tax to the recipients under the GST regime. Moreover, the DGAP has observed that Section 171 simply did not provide a supplier of any goods or services, any other means of passing on the benefit of input tax credit or reduction in rate of tax to the consumers.

7. The DGAP has noticed from the invoices made available by the Respondent that the Respondent had increased the base prices of “the subject goods” when the rate of GST was reduced from 28% to 18% w.e.f. 15.11.2017. so that the commensurate benefit of GST rate reduction was not passed on to the recipients. The DGAP has thus observed that the base prices of the subject goods were increased by the Respondent when there was a reduction in the GST rate from 28% to 18% w.e.f. 15.11.2017, so that the benefit of such reduction in GST rate was not passed on to the recipients by way of commensurate reduction in price. The DGAP has further informed that the methodology adopted for determining the amount of profiteering can be explained by illustrating the calculation in respect of specific item i.e. “Eclat Serum 30GM” sold during the month of November, 2017 (pre GST rate reduction). An average base price (after discount) was obtained on dividing the total taxable value by total quantity of this item sold during the period 01.11.2017 to 14.11.2017. The average base price of this item was compared with the actual selling price of same item sold during post-GST rate reduction i.e. on or after 15.11.2017 as illustrated in the Table-A below:-

8. The DGAP has claimed from the above Table that the Respondent has not reduced the selling price of the “Eclat Serum 30GM”, when the GST rate was reduced from 28% to 18% w.e.f. 15.11.2017, vide Notification No. 41/2017 Central Tax (Rate) dated 14.11.2017 and hence profiteered an amount of Rs. 1000/- on a particular Invoice No. 000907 dated 29.09.2018 and thus the benefit of reduction in GST rate was not passed on to the recipients by way of commensurate reduction in the price, in terms of Section 171 of the Central Goods and Services Tax Act, 2017. The DGAP, on the basis of aforesaid calculation as illustrated in Table A above, has found that profiteering in case of all goods impacted by the GST rate reduction vide Notification No. 41/2017 Central Tax (Rate) dated 14.11.2017, supplied by the Respondent during the period 15,11.2017 to 30.09.2019 has also been arrived in similar way.

8. The DGAP has claimed from the above Table that the Respondent has not reduced the selling price of the “Eclat Serum 30GM”, when the GST rate was reduced from 28% to 18% w.e.f. 15.11.2017, vide Notification No. 41/2017 Central Tax (Rate) dated 14.11.2017 and hence profiteered an amount of Rs. 1000/- on a particular Invoice No. 000907 dated 29.09.2018 and thus the benefit of reduction in GST rate was not passed on to the recipients by way of commensurate reduction in the price, in terms of Section 171 of the Central Goods and Services Tax Act, 2017. The DGAP, on the basis of aforesaid calculation as illustrated in Table A above, has found that profiteering in case of all goods impacted by the GST rate reduction vide Notification No. 41/2017 Central Tax (Rate) dated 14.11.2017, supplied by the Respondent during the period 15,11.2017 to 30.09.2019 has also been arrived in similar way.

9. The DGAP has further reported that based on the aforesaid pre and post-reduction GST rates and the details of outward taxable supplies (other than zero rated, nil rated and exempted supplies) of the impacted goods during the period 15.11.2017 to 30.09.2019, as furnished by the Respondent, the amount of net higher sales realization due to increase in the base prices of the impacted goods, despite the reduction in the GST rate from 28% to 18% or in other words, the profiteered amount came to Rs. 1,54,138/-. The amount of Rs. 1,54,138/- included Rs. 1000/- as profiteering amount collected by the Respondent from the Applicant No. 1 by selling 05 units (billed quantities) of the product “Eclat Serum” on 29.09.2018, vide Invoice No. 000907. The DGAP has furnished the details of the computation as given in the Annexure-12 of the DGAP’s Report dated 23.03.2020. The profiteered amount has been arrived at by comparing the average of the base prices of the impacted goods sold during the period 01.11.2017 to 14.11.2017 and if sale of any particular good/item was not found during this period then, in that case, the base price of that particular good/item was arrived by taking the sales of that particular good/item during previous months in a sequential manner beginning from October, 2017, if the same was not found then previous month i.e. September, 2017 and so on upto July, 2017 and then compared with the actual invoice-wise base prices of such products sold during the period 15.11.2017 to 30.09.2019, There were 23 products/goods which were impacted or on which rate of GST was reduced from 28% to 18% vide Notification No. 41/2017 Central Tax (Rate) dated 14.11.2017. out which 03 impacted goods were sold in both pre-rate reduction period as well as post rate reduction period and out of the remaining 20, for 19 impacted goods there was no sale in pre-rate reduction period and for 01 impacted good there was no sale in post rate reduction period, therefore those 20 products did not form part of profiteering calculation. The profiteering was calculated on the said 03 products which has been shown below in Table- “B”. The DGAP has further intimated that the Respondent by increasing the base prices of the impacted goods had collected excess GST from the recipients, which was also included in the above profiteered amount as the excess price collected from the recipients also included the GST charged on the increased base price. The DGAP has observed that the Respondent had made the supply of the impacted goods in the State of Maharashtra only:-

10. The DGAP has concluded that the allegation of the Applicant No.1 was that the base prices of the subject goods were increased when there was a reduction in the GST rate from 28% to 18% w.e.f. 15 11.2017. The benefit of such reduction in GST rate was not passed on to the recipients by way of commensurate reduction in price. The DGAP has also observed that the allegation of profiteering by way of increasing the base prices of the products w.e.f. 15.11.2017 was sustainable against the Respondent as have been furnished in Annexure-12 Thus, by increasing the base prices of the goods subsequent to reduction in the GST rate, the commensurate benefit of reduction in the GST rate from 28% to 18%, was not passed on to the recipients. The DGAP has further informed that the total amount of profiteering on account of contravention of the provisions of Section 171 of the Central Goods and Service Tax Act, 2017 covering the period 15.11.2017 to 30.09.2019. was Rs. 1,54,138/- that also included Rs. 1000/- as profiteering amount collected by the Respondent from the Applicant No. 1.

11. The above Report was considered by this Authority in its meeting 20.04.2020 and the Respondent was issued a notice on 01.05.2020 to explain why the above Report of the DGAP should not be accepted and his liability for violating the provisions of Section 171 of the CGST Act, 2017 should not be fixed and the Respondent and Applicant No.1 were asked to appear before the Authority on 25.05.2020. However, the hearing could not be held due to Covid-19 pandemic situation.

Thereafter, before the Order could be passed, one of the Technical Members of the Authority who had heard the matter was transferred out and thereafter the Chairman of the Authority had also left the Authority, Since, the quorum of the Authority of minimum three Members, as provided under Rule 134 was not available till 23.02.2022, the matter was not decided. With the joining of two new Technical Members in February 2022, the quorum of the Authority was restored from 23.02.2022 and the personal hearing in the matter was accorded to the Applicant No. 1 on 14.03.2022 via video-conferencing. The Applicant No. 1 did not appear in hearing and vide email dated 14.03.2022 has stated that she had received the payment of profiteered amount and matter might be considered closed from her end. Subsequently, the personal hearing in the matter was accorded to the Respondent on 31.03.2022 via video-conferencing. During the hearing, the Respondent has stated that the rate reduction benefit was not passed on to him by his supplier while supplying the product “Eclat Serum” to him. 12. Meanwhile, the parties were directed to file their submissions via email.

Thereafter, the Respondent vide his email dated 14.09.2020 has agreed to pay the profiteered amount as computed by the DGAP in his Report dated 23.03.2020. Hence, the DGAP was directed to provide necessary guidance to the Respondent so that he could pay the above amount.

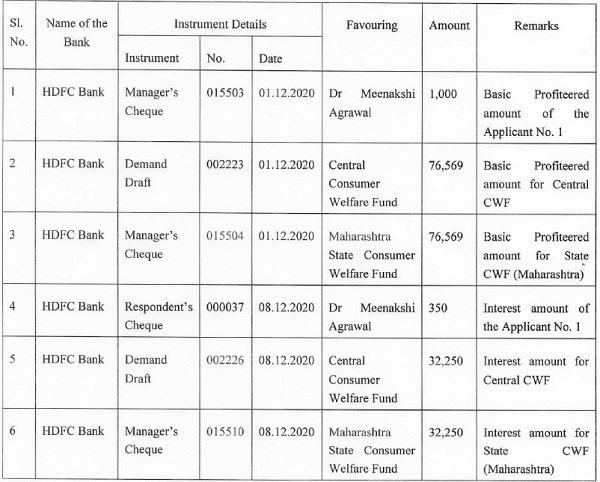

The DGAP vide letter dated 15.12.2020 has asserted that the Respondent had issued the Demand Drafts (DDs) on 01.12.2020 for payment of Rs. 1000/- to the Applicant No. 1 and Rs. 76,569/- to Central Consumer Welfare Fund (CWF) and Maharashtra State CWF each.

Therefore, the DGAP vide email dated 02.12.2020 asked the Respondent to remit the interest amount also and furnish all the documentary evidence to the DGAP. In compliance, the Respondent vide email dated 09.12.2020 has furnished the copies of 6 Cheques/ Demand Drafts as detailed below:-

13. The DGAP has further verified that the Respondent had submitted copies of the acknowledgements received from the Applicant No. 1 vide email dated 09.12.2020. However, an email was sent to the Applicant No. 1 on 09.12.2020. The Applicant No. 1 vide email dated 11.12.2020 had confirmed the receipt of Rs. 1,000/- and Rs. 350/- from the Respondent.

14. The DGAP has also stated that in respect of Central CWF, the Respondent had submitted copies of the Demand Drafts of Rs. 76,569/- and Rs. 32,250/- for payment of basic profiteered amount and interest amount respectively and has informed that he had sent these drafts to the Pay and Accounts Officer, Consumer Welfare Fund, Department of Consumer Affairs, New Delhi through courier. In this regard, an email was sent on 12.12.2020 to the Pay and Accounts Officer, CWF, Department of Consumer Affairs, New Delhi for confirmation of the receipt of said 2 Demand Drafts from the Respondent. The Sr. Accounts Officer, Pay and Accounts Office, Department of Consumer Affairs, New Delhi, vide email dated 14.12.2020 informed that DD/Cheque No. 002223 for Rs. 76,569/- has been deposited in the bank and other DD/Cheque No. 002226 for Rs.32 250 has been returned to the Respondent as cheque favouring was not correct. The DGAP has also intimated that the Respondent has further informed that the Demand Draft No. 002226 dated 08.12.2020 for Rs.32,250/- favouring “Central Consumer Welfare Fund” has again been submitted by him to the PAO. Consumer Welfare Fund, New Delhi. In this regard, an email was sent on 21.01.2021 to the Pay and Accounts Officer, CWF, Department of Consumer Affairs, New Delhi for confirmation of the receipt of the above Demand Draft from the Respondent. Further, reminder email was also sent on 25.01.2021 to the PAO, CWF, New Delhi. Thereafter, the DGAP has confirmed that the Respondent has submitted a correct Demand Draft No. 002229 dated 16.01.2021 amounting to Rs. 32,250/- in the above office which has been deposited in the Fund’s Account vide Challan No. 059 dated 20.01.2021. Hence, the Respondent has remitted entire profiteered amount along with applicable interest.

15. The DGAP has also stated that in respect of Maharashtra State Consumer Welfare Fund, the Respondent vide his email dated 20.01.2021 submitted that he had submitted two Demand Drafts bearing No. 015540 & 015541 both dated 19.12.2020 for Rs. 32,250/- and 76,569/- favouring “Maharashtra State Consumer Welfare Fund” to the State GST Office, Mazgaon, Mumbai and got the acknowledgement of the same which was forwarded by the Respondent as attachment to the email dated 20.01.2021. The DGAP vide email dated 21.01.2021, requested the State GST Office, Mazgaon, Mumbai for confirmation of the deposition of above amounts in the Consumer Welfare Fund (Maharashtra State). Dr. Pramod B. Bhosale, Dy. Commissioner of State Tax, HQ-7, SME-GST Refunds, GST Bhavan, Mazgaon, Mumbai, vide email dated 25.01.2021, confirmed that the two Demand Drafts amounting Rs. 32,250/- and Rs. 76,569/- submitted by the Respondent, had been deposited in CWF Account under GST (Maharashtra State) in RBI Mumbai on 11.01.2021 and amount has been credited into the account. Hence, the DGAP has confirmed that the basic profiteered amount of Rs. 76,569/- along with interest of Rs. 32,250/- has been deposited in the State Consumer Welfare Fund (Maharashtra State) by the Respondent.

16. We have carefully considered the Reports of the DGAP, the submissions made by the Respondent and the material placed on record. On examining the various submissions we find that the following issues need to be addressed in the present case:-

a. Whether the Respondent was required to pass on and has passed on the commensurate benefit of reduction in the rate of tax to his customers?

b. Whether there was any violation of the provisions of Section 171 (1) of the CGST Act. 2017 in this case?

17. In this connection perusal of Section 171 of the CGST Act shows that it provides as under:-

“(1). Any reduction in rate of tax on any supply of goods or services or the benefit of input tax credit shall be passed on to the recipient by way of commensurate reduction in prices.

(2). The Central Government may, on recommendations of the Council, by notification, constitute an Authority, or empower an existing Authority constituted under any law for the time being in force, to examine whether input tax credits availed by any registered person or the reduction in the tax rate have actually resulted in a commensurate reduction in the price of the goods or services or both supplied by him.”

(3). The Authority referred to in sub-section (2) shall exercise such powers and discharge such functions as may be prescribed.

(3A) Where the Authority referred to in sub-section (2) after holding examination as required under the said sub-section comes to the conclusion that any registered person has profiteered under subsection (1), such person shall be liable to pay penalty equivalent to ten per cent. of the amount so profiteered.

PROVIDED that no penalty shall be leviable if the profiteered amount is deposited within thirty days of the date of passing of the order by the Authority.

Explanation:- For the purpose of this section, the expression “profiteered” shall mean the amount determined on account of not passing the benefit of reduction in rate of tax on supply of goods or services or both or the benefit of input tax credit to the recipient by way of commensurate reduction in the price of the goods or services of both.”

18. It is also observed from the record that the Respondent is engaged in selling of medicines from his retail stores having GSTIN 27BDVPM0061N1ZZ. It is also revealed from the plain reading of Section 171 (1) supra that it deals with two situations one relating to the passing on the benefit of reduction in the rate of tax and the second about the passing on the benefit of the ITC. On the issue of reduction in the tax rate, it is apparent from the record that there has been a reduction in the rate of tax from 28% to 18% w.e.f. 15.11.2017, on “the subject goods” being supplied by the Respondent, vide Notification No. 41/2017-Central Tax (Rate) dated 14.11.2017. Therefore, the Respondent is liable to pass on the benefit of tax reduction to his customers in terms of Section 171 (1) of the above Act. It is also apparent that the DGAP has carried out the present investigation w.e.f. 15.11.2017 to 30.09.2019.

19. It is also evident that the Respondent has been selling “the subject goods” etc. during the period from 15.11.2017 to 30.09.2019 to his customers. Upon comparing the average base prices as per the details of sale transactions submitted by the Respondent for the pre rate reduction period from 01.11.2017 to 14.11.2017 and the actual base prices post rate reduction w.e.f. 15.11.2017 to 30.09.2019 it has been found that the GST rate of 18% has been charged by the Respondent w.e.f. 01.01.2019, however, the base prices of the products have been increased more than their pre rate reduction base prices, w.e.f. 15.11.2017 which shows that because of the increase in the base prices the cum-tax prices paid by the consumers were not reduced commensurately, inspite of the reduction in the GST rate. On the basis of the aforesaid pre and post reduction GST rates and the details of the outward supplies (other than zero rated, nil rated and exempted supplies) made during the period from 15.11.2017 to 30.09.2019, the amount of net higher sale realization due to increase in the base prices of the products, despite the reduction in the GST rate from 28% to 18% or the profiteered amount has come to Rs. 1,54,138/- (inclusive of Rs. 1000/- of the Applicant No. 1) including the GST on the base profiteered amount. The details of the computation have been given by the DGAP in Annexure-12 of his Report dated 23.03.2020.

20. From the above facts and discussion, it is evident that, the Respondent did not reduce the selling price of the products mentioned above when the GST rate was reduced from 28% to 18% w.e.f. 15.11.2017 and hence, the benefit of reduction in GST rate was not passed on to the recipients by way of commensurate reduction in the prices, in terms of Section 171 of the CGST Act, 2017 and therefore, he has contravened the provisions of Section 171 of the CGST Act, 2017.

21. Based on the above facts, it is established that the Respondent has acted in contravention of the provisions of Section 171 of the CGST Act, 2017, and has not passed on the benefit of reduction in the rate of tax to his recipients by commensurate reduction in the prices. Accordingly, the profiteered amount is determined as Rs. 1,54,138/- as per the provisions of Rule 133 (1) of the CGST Rules 2017. The Respondent is therefore directed to reduce the prices of his products as per the provisions of Rule 133 (3) (a) of the CGST Rules, 2017, keeping in view the reduction in the rate of tax so that the benefit is passed on to the recipients. Accordingly, the Respondent is required to deposit the profiteered amount of Rs. 1,54,138/- along with the interest to be calculated @ 18% from the date when the above amount was collected by him from the recipients till the above amount is deposited in terms of Rule 133 (3) (b) of the CGST Rules, 2017. Since the other recipients (other than the Applicant No. 1), in this case, are not identifiable, the Respondent is directed to deposit the amount of profiteering of Rs. 1,53,138/- along with interest in the CWFs of the Central and Maharashtra State Government as per the provisions of Rule 133 (3) (c) of the CGST Rules, 2017 in the ratio of 50:50 along with interest @ 18% till the same is deposited.

22. The DGAP has verified that the Applicant No. 1 vide email dated 11.12.2020 had also confirmed the receipt of the profiteered amount of Rs. 1,000/- along with interest of Rs. 350/- from the Respondent. In respect of Maharashtra State CWF, the DGAP has confirmed that the Respondent has submitted the Demand Draft No. 015504 dated 01.12.2020 of Rs. 76,569/- for payment of the profiteered amount and Demand Draft No. 015510 dated 08.12.2020 of Rs. 32,250/- for payment of the interest amount to the Dy. Commissioner of State Tax, GST Bhavan, Mazgaon, Mumbai, which has been deposited in CWF Account under GST (Maharashtra State) in RBI Mumbai on 11.01.2021 and the above amounts have been credited into the account. Hence, the DGAP has verified that the basic profiteered amount of Rs. 76,569/- along with interest of Rs. 32,250/- has been deposited in the Maharashtra State Consumer Welfare Fund by the Respondent.

23. With regard to Central CWF, the DGAP has further confirmed that the Respondent has submitted the Demand Draft No. 002223 dated 01.12.2020 of Rs. 76,569/- for payment of the profiteered amount and Demand Draft No. 002229 dated 16.01.2021 of Rs. 32,250/- for payment of interest amount to the Sr, Accounts Officer, Pay and Accounts Office, Department of Consumer Affairs, New Delhi, which has been deposited in the Fund’s Account vide Challan No. 059 dated 20.01.2021 which has been taken on record. The Respondent has paid the entire profiteered amount of Rs. 1,54,138/- along with interest @ 18% of Rs. 64,850/- for the investigation period from 15.11.2017 to 30.09.2019.

24. Based on the above facts it is clear that the Respondent has contravened the provisions of Section 171 (1) of the CGST Act, 2017. However, since, the penalty prescribed under Section 171 (3A) of the CGST Act, 2017 for violation of the above provisions has come in to force w.e.f. 01.01.2020 and the infringement pertains to the period from 01.01.2019 to 30.09.2019 and the Respondent has also deposited the profiteered amount alongwith the interest, therefore, no penalty is proposed to be imposed on the Respondent.

14. Further, during the hearing held on 31.03.2022, the Respondent has stated that the rate reduction benefit was not passed on to him by his supplier/s while supplying the product “Eclat Serum” to him, Therefore, there arises a need to check whether his supplier has passed on the above benefit to him or not so that the investigation can be taken to its logical end in terms of Section 171 of the CGST Act, 2017 and the Rules framed thereunder. Accordingly, this Authority directs the DGAP to gather the information of the Respondent’s supplier/s from the Respondent and investigate the entire supply chain under Rule 133(5) of the CGST Rules, 2017 and submit the investigation report within 3 months of passing of this order.

25. As per the provisions of Rule 133 (1) of the CGST Rules, 2017 this order was required to be passed within a period of 6 months from the date of receipt of the Report from the DGAP under Rule 129 (6) of the above Rules. Since, the present Report has been received by this Authority on 16.04.2020 the order was to be passed on or before 15.10.2020. However, due to prevalent pandemic of COVID-19 in the Country this order could not be passed on or before the above date. In this regard it would be relevant to mention that the Hon’ble Supreme Court in Miscellaneous Application No 21 of 2022 in MA 665 of 2021 in Suo Moto Writ Petition (C) No. 03/2020 vide its Order dated 10.1.2022 has directed that:-

” I. The order dated 23.03.2020 is restored and in continuation of the subsequent orders dated 08.03.2021, 27,04.2021 and 23.09.2021, it 1:5′ directed that the period from 1103,2020 till 28.02.2022 shall stand excluded for the purposes of limitation as may be prescribed under any general or special laws in respect of all judicial or quasi-judicial proceedings.

II. Consequently, the balance period of limitation remaining as on 03.10.2021, if any, shall become available with effect from 01.03.2022.

III. In cases where the limitation would have expired during the period between 15.03.2020 till 28.02.2022, notwithstanding the actual balance period of limitation remaining, all persons shall have a limitation period of 90 days from 01.03.2022. In the event the actual balance period of limitation remaining, with effect from 01.03.2022 is greater than 90 days, the longer period shall apply.

IV. It is further clarified that the period from 15.03.2020 till 28.02.2022 shall also stand excluded in computing the periods prescribed under Section 23(4) and 29A of the Arbitration and Conciliation Act, 1996, Section 12A of the Commercial Courts Act, 2015 and provisos (b) and (c) of Section 138 of the Negotiable Instruments Act, 1881 and any other laws, which prescribe period(s) of limitation for instituting proceedings, outer limits (within which the court or tribunal can condone delay) and termination of proceedings’

Therefore, the present order is being passed within the period of limitation as allowed by the hon’ble Supreme Court,

26. A copy each of this order be supplied to the Applicants, the Respondent and to the concerned Commissioners CGST /SGST for necessary action. File be consigned after completion.